The Leapfrog Doctrine: How China Systematically Conquered Every Technology It Targeted

Table of Contents

Author’s Note: This is the first article in a multi-part series examining whether China can achieve dominance in quantum computing — the technology that may ultimately determine the balance of global power in the 21st century.

My thesis is direct: China will likely win the quantum race. Not because it has better scientists or more qubits today, but because of a convergence of structural advantages that Western analysts consistently underestimate — a proven industrial strategy I call the Leapfrog Doctrine, unprecedented coordinated investment across public and private sectors, a lack of Western visibility into the true scale and status of Chinese quantum programs, an energy and digital infrastructure without parallel, and the adaptive resilience that turns every Western restriction into an accelerant for self-sufficiency.

This article establishes the foundation. It documents the Leapfrog Doctrine across eight sectors, drawing on data, lived experience, and two decades of watching China’s technological transformation from factory floors in Dongguan to boardrooms in London. The companion articles will turn to quantum directly — examining what China has already achieved, what it is concealing, how its whole-of-nation approach differs from fragmented Western efforts, and why the comfortable assumption that the West leads may be the most dangerous strategic miscalculation of our time.

The series has been several months in the making. I hope it challenges assumptions — especially comfortable ones.

Introduction

Almost fifteen years ago, I stood on the mezzanine floor of a manufacturing facility in Dongguan, staring into the dark. Literally.

Below me, a sprawling production line hummed with the rhythmic, pneumatic hiss of assembly arms and the whine of servos. There were no overhead lights. There were no workers on the line. There was only the glow of status LEDs blinking in the gloom, painting the polished concrete floor in shifting hues of green and amber. I was working on some of the early “dark factory” implementations – fully automated systems designed to operate 24/7 without human intervention – at a time when Western manufacturing only started debating the ethics of replacing a single worker with a Baxter robot. (This was the genesis of my book, The Future of Leadership in the Age of AI, written a decade ago with Luka Ivezic).

This was not the China of cheap plastic toys and sweatshops that dominated Western headline. This was a China that was already silently, methodically, and ruthlessly climbing the value chain. Even then, over a decade ago, the technological disparity in daily life was jarring. I remember returning to London or San Francisco and feeling like I had traveled back in time. In Shanghai, I paid for my morning coffee with a WeChat, split a dinner bill instantly with friends, and booked a doctor’s appointment on an app. In the West, I was still signing paper receipts, writing cheques, and fumbling with chip-and-pin machines that worked half the time.

The apartments I visited in Shenzhen featured smart integration – facial recognition entry, automated climate control, integrated delivery lockers, automated sun shades and mood lighting that maintained user’s preference throughout the day, robotic vacuums that automatically activated when all the residents are out of the apartment, and so on – all controlled through a building-specific mobile app. Features that came by default with every new unit built, and which would be marketed as “cutting-edge luxury” in New York even today.

Yet, when I returned to the boardroom discussions in Europe and North America, the narrative remained stubbornly, dangerously frozen in 1990. “China steals IP,” the executives would say, swirling their wine. “They can’t innovate. They can only copy.“

This cognitive dissonance has been the West’s greatest strategic failure of the 21st century.

The data now confirms what I saw on those factory floors fifteen years ago. The Australian Strategic Policy Institute’s Critical Technology Tracker, updated in March 2026, found that China leads in 69 of 74 critical technologies tracked — up from just 3 of 64 in the 2003–2007 period. The United States maintains its edge in only 5. Forty-one of those technologies are now at what ASPI calls “high monopoly risk,” meaning China publishes over three times the high-impact research of its nearest competitor and hosts eight or more of the top ten global institutions. The Information Technology and Innovation Foundation, after a 20-month investigation across 10 advanced-technology industries, concluded that China is “not a tiger, but rather a fire-breathing dragon on government-provided steroids.” ITIF President Robert Atkinson warned that for the first time in over a century, America faces an adversary that can outproduce it — and will likely soon be able to out-innovate it.

The Nature Index for 2025 shows that China overtook the United States in contributions to 145 elite scientific journals, with the lead expanding sharply — more than quadrupling in a single year. The Chinese Academy of Sciences has held the number-one global institution ranking for thirteen consecutive years — with more than double the output of second-placed Harvard. Georgetown University’s Center for Security and Emerging Technology projects that Chinese universities are now graduating more than 77,000 STEM PhDs per year, compared with roughly 40,000 in the United States. It leads globally in PCT patent filings with 70,160 applications in 2024, a position it has held since 2019.

These measurements describe a world that most Western boardrooms and policy offices have not yet internalized.

For the last twenty years, I have argued that we are drastically underestimating the People’s Republic. We have been fighting a mental image of a rival that ceased to exist years ago. The “copycat” era was merely the tuition fee China paid to learn the game. Today, they are not just playing the game; they are rewriting the rules.

The Strategic Balance: US vs. China

2025 Assessment of Critical Technologies

- Lead in LLM/Generative Models

- Advanced Quantum Hardware Design

- Dominance in Robotics & Physical AI

- Quantum Communications & Energy Grid

Why We Can No Longer Ignore China

To understand how China achieved this position, we must first dismantle the lingering myth of “Made in China” inferiority. For decades, Western narratives around China’s tech development were dominated by two themes: copying and cheap labor. China was the place that made your iPhone or your T-shirt more cheaply, often by “stealing” intellectual property or churning out knock-offs. That image is hopelessly outdated. Since 2010s, China has transformed into a global R&D leader, an innovator, and a quality manufacturer – in many cases on par with or ahead of Western nations. The trajectory of the Chinese technological engine is not linear; it is exponential, driven by a series of “Sputnik moments” that the West has largely chosen to ignore until it was too late.

The evidence is no longer anecdotal; it is undeniable. From the shock release of the Huawei Mate 60 Pro to the recent capabilities of DeepSeek, China is systematically out-innovating expectations. But while 5G, EVs, and AI draw the headlines, a more profound shift is occurring – one that will define the fundamental architecture of global power in the 21st century.

We are standing at a technological inflection point, and we must confront a stark reality: China is winning the technological cold war across virtually every frontier that matters.

This article is not an endorsement of the Chinese political system, nor is it a piece of ideological propaganda. It is a pragmatic analysis based on cold, hard data and lived experience. My goal is to correct persistent Western misconceptions that, left unchallenged, will produce strategic blindness at precisely the moment clarity is most needed.

One more observation from my consulting work is worth sharing. One of the most common questions I am now being asked in my Applied Quantum practice — from CISOs and CTOs across Europe and Asia — is how their organizations can develop and maintain access to quantum computing that is not dependent on the United States. Nobody is yet considering Chinese quantum tech as the alternative. But it is telling — and historically significant — that US technology, which was always the safe default, is now being actively avoided in many countries’ strategic planning. That shift in sentiment is itself a leading indicator of where the balance of technological power is heading.

I will address the quantum dimension in detail in a companion article. But the quantum race cannot be understood in isolation. It must be understood as the latest — and potentially most consequential — manifestation of a pattern that has already played out across electric vehicles, telecommunications, robotics, drones, energy, semiconductors, and artificial intelligence. That pattern is what I call the Leapfrog Doctrine.

In the chapters that follow, we will first examine that playbook in detail — the five stages, the timeline, the evidence. We will then trace its execution across eight sectors: automotive, telecommunications, robotics, drones, energy infrastructure, digital integration, semiconductors, and artificial intelligence. Each tells the same story from a different angle. Each demonstrates the same strategic logic producing the same outcome. And each raises the same question: if the pattern has never failed, what reason do we have to believe it will fail in quantum computing — the technology that may matter more than all the others combined?

If the West does not catch up to the reality of China’s capabilities, it risks being blindsided in a competition that it still mistakenly thinks it has in the bag. The “dark factories” of Dongguan were just the beginning; the Quantum Age is where the real battle will be decided. But to understand why, we must first examine the track record.

The Leapfrog Doctrine – China’s Strategic Playbook

Before we examine the individual sectors where China has achieved or is approaching dominance, it is worth understanding the strategic logic that connects them. Because these are not isolated victories. They are the output of a repeatable, documented, and — in retrospect — almost mechanical process.

The concept of technological leapfrogging has been discussed in development economics since Brezis, Krugman, and Tsiddon’s seminal 1993 work on cycles in national technology leadership — originally describing how developing nations could skip intermediate technologies entirely, moving from no telephones to mobile phones, bypassing landlines. What China has done is industrialize this concept into a national strategy, applying it systematically across sectors with a consistency that suggests not luck, but doctrine. The Leapfrog Doctrine.

The playbook has five stages. Every sector covered in this article follows them.

Stage 1: Strategic Selection. Beijing identifies a technology that is either transitioning between paradigms (ICE to electric, 4G to 5G, classical to quantum) or where incumbent leaders have accumulated technical debt that creates an opening. The key insight is timing: China does not try to catch up in mature technologies where Western firms have insuperable advantages. Instead, it identifies the next wave and places the bet before the wave breaks. Electric vehicles were prioritized precisely because China could never close the gap in internal combustion engine technology — a century of accumulated German, Japanese, and American expertise in precision machining, metallurgy, and engine tuning. But by betting on electrification, Beijing made that century of expertise largely irrelevant.

Stage 2: Coordinated Investment. The selected technology is embedded into Five-Year Plans, receives dedicated funding through national programs, provincial initiatives, and state-owned enterprise mandates. The investment is not just financial — it includes regulatory support, infrastructure buildout, talent pipeline creation, and guaranteed domestic market access. The scale is typically staggering: $1.4 trillion for 5G networks, $15 billion (at minimum) for quantum technologies, hundreds of billions for clean energy. Provincial and municipal governments compete to attract designated industries, creating clusters — Hefei for quantum, Shenzhen for drones and electronics, Shanghai for autonomous vehicles — that generate agglomeration effects.

Stage 3: Protected Scaling. Domestic champions are given a massive home market in which to iterate, fail, improve, and scale. This phase often looks messy from the outside — hundreds of EV startups, dozens of drone makers, scores of quantum companies competing ferociously. Western observers frequently mistake this chaos for waste. It is not waste. It is Darwinian selection at industrial scale, producing survivors that are battle-hardened by competition far more intense than anything they will face in global markets. BYD survived a brutal domestic EV shakeout that eliminated hundreds of competitors. DJI emerged from a Shenzhen ecosystem that incubated dozens of drone startups. The winners are forged in fire.

Stage 4: Cost Destruction. Through vertical integration, massive production volumes, and supply chain control, Chinese firms drive costs below what Western competitors can match. The BYD Seagull starts under $10,000. Unitree’s G1 humanoid costs $16,000 versus $100,000+ for Western equivalents. Chinese solar panels have been driven below $0.10/W. DJI drones cost one-eighth to one-fourteenth of Pentagon-approved American alternatives. This cost destruction is not primarily about cheap labor — it is about scale, integration, and the accumulated efficiencies of producing millions of units. Morgan Stanley’s analysis of humanoid robot Bills of Materials found that sourcing components from the Chinese supply chain costs $46,000 versus $131,000 from non-Chinese sources — a “China Discount” of $85,000 per robot that reflects industrial clustering, not wage arbitrage.

Stage 5: Global Market Capture. Armed with superior products at lower prices, Chinese firms expand internationally — first into the Global South (Belt and Road markets, ASEAN, Africa, Latin America), then into Europe, and ultimately into direct competition with Western incumbents even in their home markets. This expansion is often accompanied by a strategic “openness” play: releasing technology for free or at minimal cost to build ecosystems and establish dependency. Origin Pilot (the quantum operating system released for free download) follows the same playbook as DeepSeek (open-source AI models) and Huawei’s 5G infrastructure packages offered to developing nations on favorable terms.

The timeline from Stage 1 to Stage 5 is remarkably consistent: approximately 10 to 20 years. High-speed rail was prioritized around 2001 and achieved global dominance by approximately 2018. EVs were designated a strategic priority in 2010 and achieved market leadership by 2024. 5G was embedded in Made in China 2025 and achieved infrastructure dominance by 2023.

The pattern has repeated across every sector examined in this article:

High-speed rail: Prioritized under the 10th Five-Year Plan (2001). Today: 50,000 km of track — 70% of the world’s total. CRRC controls 73% of the global metro rolling stock market. The CR450 prototype operates at 450 km/h. Timeline to dominance: ~15 years.

Solar panels: Designated in the 2010 Strategic Emerging Industries plan. Today: approximately 93% of global polysilicon, 97% of wafers, 80%+ of cells and modules. Nine of the top 10 polysilicon manufacturers are Chinese. Module prices driven below $0.10/W. Timeline to dominance: ~12 years.

Wind turbines: Included in the 2010 Strategic Emerging Industries plan. In 2025, Chinese turbine makers took the top six global positions for the first time. Vestas slipped to seventh — its first time outside the top five since rankings began. China became the first market to add over 100 GW of wind capacity in a single year. Timeline to dominance: ~13 years.

Shipbuilding: Strategic priority across multiple FYPs. China now accounts for 53.3% of global output and approximately 75% of new global orders. The U.S.-China Economic and Security Review Commission noted that China State Shipbuilding Corporation alone produced more commercial vessels by tonnage in one year than the United States has since the end of World War II.

Rare earths: Strategically prioritized since at least the 10th FYP era. China controls approximately 60% of global mining, 90% of separation and refining, and 94% of sintered permanent magnets. In April 2025, China imposed export controls on seven rare earth elements, causing magnet shipments to fall 74% — demonstrating willingness to use resource control as strategic leverage.

The question for quantum computing is not whether this pattern can apply. It is whether anything has changed to prevent it from applying. As we will see, the answer is: nothing has changed. If anything, the conditions are more favorable for China in quantum than in any previous sector.

But first, let us examine the sectors in detail.

The Leapfrog Doctrine in Action

From Imitation to Dominance: The Auto Industry Precedent

Consider the auto industry. It wasn’t long ago that Chinese cars were derided as low-quality imitations. Today, that joke “has long worn thin” notes the Guardian, underscoring how Chinese automakers have upped their game in design, safety, and technology. China has surpassed Japan as the world’s largest car exporter, and its EV brands are making serious inroads into Europe.

Western industry titans are finally, albeit belatedly, acknowledging this. Ford CEO Jim Farley recently described his tour of Chinese auto plants as “the most humbling thing I’ve ever seen,” warning that if Western firms lose the EV race to the superior quality and automation of Chinese manufacturing, “we do not have a future.” As reported by the Centre for European Reform, executives are coming back “terrified,” describing factories so automated that lights are unnecessary, run by “a tremendous number of highly skilled, educated engineers who are innovating like mad.”

Market Dynamics

In Western Europe, Chinese cars outsold Korean brands for the first time in late 2025, and Britons are buying Chinese EVs by the hundreds of thousands. These vehicles come packed with features – from advanced driver assist systems to plush tech-infused interiors – often at a price point Western competitors struggle to match.

Far from being knock-offs, brands like BYD, NIO, Xpeng, Geely, even Xiaomi (yes, the mobile phone maker), and others are now leading in electric drivetrain technology and innovative business models (for example, battery swapping services for EVs).

Once relegated to the role of a manufacturing backwater or a lucrative market for Western joint ventures, China has methodically engineered a domestic auto industry that is now the world’s largest and, by many metrics, its most advanced.

The prevailing narrative in Western capitals and boardrooms has shifted from dismissal to alarm. The “fast follower” has become the “pace setter.” This evolution was not accidental. Recognizing early in the 21st century that its domestic manufacturers could likely never close the engineering gap with German, Japanese, and American incumbents in complex internal combustion engine technology, China’s industrial planners opted for the “leapfrog” strategy described above. By betting the national industrial base on the next technological wave – electrification, connectivity, and autonomy – China effectively rendered the century of accumulated ICE expertise held by legacy automakers less relevant.

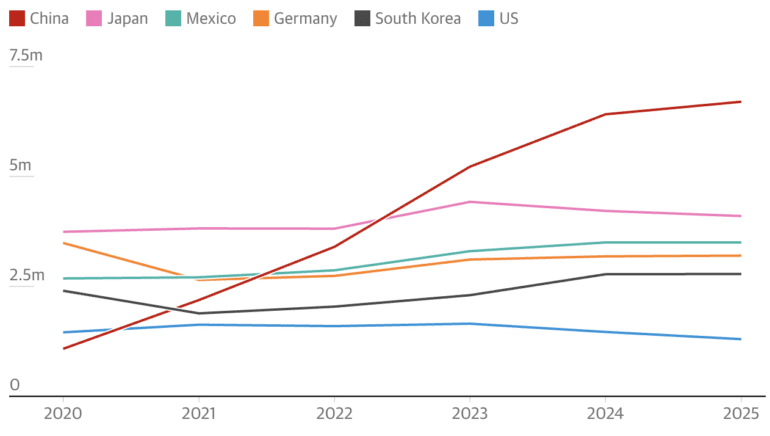

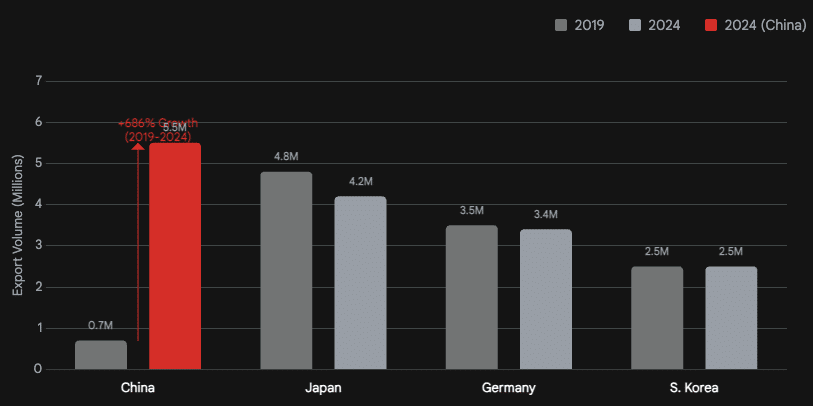

The most visible manifestation of China’s automotive maturation is the unprecedented surge in exports. In 2019, China exported a modest 0.7 million vehicles, a figure that barely registered on the global stage dominated by Japan and Germany. By the close of 2023, that figure had skyrocketed to 4.91 million, and in 2024, exports reached nearly 6 million vehicles (specifically 5.86 to 5.9 million depending on the specific dataset utilized). This 19.3% year-on-year increase in 2024 solidified China’s position as the world’s number one auto exporter, surpassing Japan.

The composition of these exports reveals a critical shift. While traditional internal combustion vehicles still comprise a volume share, the growth engine is unquestionably New Energy Vehicles (NEVs). In 2024, NEV exports reached approximately 1.3 million units, with some data sources indicating NEV exports surging by 90% in the first ten months of the year alone. This is not merely a volume game; it is a value game. The average export price of a Chinese car has risen from $14,500 in 2020 to $18,300 in 2024, reflecting a move upmarket into higher-quality, feature-rich intelligent vehicles.

The competitive landscape of global exports has been fundamentally reordered. In 2019, Japan led with 4.8 million units, followed by Germany at 3.5 million. By 2024, China stood at 5.5 million, pushing Japan to second place (4.2 million) and Germany to third (3.4 million). This rearrangement is not a temporary fluctuation but a structural realignment driven by China’s dominance in the high-growth EV segment, which now accounts for over 20% of global car sales.

The latest data is even more striking. BYD sold 4,602,436 NEVs in 2025, including 2,256,714 pure battery-electric vehicles — outselling Tesla’s 1,636,129 BEVs by over 620,000 units. This marked the first full calendar year that BYD surpassed Tesla in electric-only sales. BYD’s overseas sales exceeded one million units for the first time, growing 150% year-over-year. By March 2026, overseas sales had reached 40% of BYD’s total monthly volume — up from negligible share just three years earlier.

Total Chinese NEV exports reached 2.62 million in 2025, approximately doubling year-over-year. Despite EU tariffs reaching up to 45.3% and US tariffs exceeding 100%, Chinese EV sales into Europe nearly doubled in 2025 — and prices did not increase. Most actually fell.

Battery Innovation

If scale is the engine of the Chinese auto industry, battery technology is the fuel. China’s dominance in the battery supply chain is absolute, accounting for over 70% of global EV production. But beyond volume, Chinese firms like CATL and BYD are driving the fundamental chemistry innovations that are resetting the cost and performance curves for the entire industry. The West is currently playing catch-up not just in manufacturing capacity, but in the fundamental science of energy storage.

China’s initial bet on Lithium Iron Phosphate (LFP) batteries – cheaper, safer, but historically less energy-dense than Nickel Manganese Cobalt (NMC) batteries favoured by the West – has paid massive dividends. Through cell-to-pack (CTP) innovations like BYD’s “Blade Battery,” Chinese engineers solved the energy density problem without sacrificing cost or safety. By eliminating expensive cobalt and nickel, Chinese manufacturers have insulated themselves from some of the most volatile commodity price swings that plague Western supply chains.

While the West focuses on solid-state batteries for premium vehicles, China is simultaneously attacking the bottom of the market with Sodium-Ion technology. This is a strategic masterstroke. Sodium is abundant and cheap, unlike lithium, and sodium-ion batteries perform significantly better in cold weather. In January 2024, JAC (a VW partner) began mass production of the Yiwei EV, the world’s first car powered by a sodium-ion battery. While the energy density (120-140 Wh/kg) is lower than lithium, it is sufficient for urban mobility and short-range commuting. This technology creates a “cost floor” that Western manufacturers simply cannot match. It allows for the production of viable EVs at price points (e.g., under $10,000) that are impossible with lithium chemistries. This technology is particularly potent for the Global South, where price sensitivity is high and charging infrastructure may be less robust, as sodium-ion allows for full discharge without damage.

At the premium end of the spectrum, China is deploying semi-solid-state batteries at a commercial scale, years ahead of Western timelines. Nio has successfully commercialized a 150 kWh semi-solid-state battery pack. In real-world testing (not just lab conditions), this battery achieved a range of over 1,000 kilometers (approx. 664 miles) on a single charge across multiple routes in China.

Sitting at the center of this ecosystem is CATL, the world’s largest battery maker. CATL is not merely a supplier but a market maker. The immense scale of Chinese battery production has driven prices down relentlessly. BloombergNEF estimates that global average lithium-ion battery pack prices fell about 20% in 2024 to $115/kWh, with pack prices in China dipping below $100/kWh. By 2025, average pack prices in China had fallen further to around $84/kWh — roughly 40% lower than in North America and Europe — giving Chinese automakers a structural cost advantage that Western startups and legacy OEMs struggle to overcome.

In March 2026, BYD unveiled its second-generation Blade Battery with Flash Charging 2.0, enabling a charge from 10% to 70% in just five minutes at a 10C rate — more than double Tesla’s best charging speed. BYD announced plans for 20,000 flash-charging stations by end of 2026, with 4,239 completed in the first two months. CATL, meanwhile, has achieved 500 Wh/kg energy density in solid-state battery testing and targets mass production for approximately 2030. A government-backed consortium received approximately $830 million for solid-state battery development, with the first national technical standard scheduled for July 2026.

“Smartphone-ification” of the Auto Plant

The rise of China’s auto industry is not just about what is being built, but how it is being built. The entry of consumer electronics giants into the automotive space has introduced a new manufacturing philosophy. The most striking example is Xiaomi, a company that transitioned from smartphones to smart cars with terrifying speed.

Xiaomi entered the auto market with the SU7 sedan and immediately redefined manufacturing benchmarks. At its Beijing “Hyperfactory,” Xiaomi produces a new SU7 every 76 seconds. This facility is not a traditional auto plant; it is a scaled-up electronics assembly line that applies consumer electronics rigor to heavy industry.

The factory utilizes “Hyper Die-Casting” (gigacasting) technology, using a proprietary titanium-based alloy to cast the entire rear underbody of the vehicle in a single shot. This replaces 72 separate stamped parts and eliminates 840 weld points. While Tesla pioneered gigacasting, Xiaomi has refined the speed and precision of the process, integrating it into a highly automated quality control system that uses X-rays and LiDAR to inspect casts with ±0.05mm accuracy. This precision allows for tighter panel gaps and higher structural rigidity, contributing to the “premium” feel of the vehicle despite its competitive price.

The level of automation in Chinese EV plants is staggering to Western observers. Xiaomi’s body shop is 100% automated for key processes, utilizing over 700 robots. The assembly line, typically the most labor-intensive part of car making, employs Autonomous Mobile Robots (AMRs) for logistics, completely replacing human forklift drivers and traditional conveyor belts in certain sections. These AMRs navigate the factory floor autonomously, delivering parts to workstations with pinpoint timing.

This stands in stark contrast to the historical advantage of Chinese manufacturing: cheap labor. The new advantage is speed and precision driven by robotics. This shift from “cheap labor” to “smart manufacturing” creates a structural cost advantage that tariffs on labor dumping cannot easily address. It implies that even if Western nations close their borders, their domestic industries may still be inefficient by comparison.

Digital Experience as Differentiator

Western automakers often view the car as a machine with a computer inside. Chinese automakers view the car as a computer with wheels. This philosophical difference has resulted in a chasm in the digital user experience (UX). The “software-defined vehicle” is not a buzzword in China; it is the baseline expectation.

The Xiaomi SU7 exemplifies this integration. The vehicle supports a “Human x Car x Home” ecosystem, where the car seamlessly connects with over 1,000 Xiaomi smart home devices. The cockpit features a 16.1-inch 3K central screen and a 56-inch Heads-Up Display (HUD). Crucially, the system is open: it supports magnetic attachment of iPads and other peripherals, effectively turning the car into a modular workspace or entertainment hub. Ford CEO Jim Farley, who personally drives a Xiaomi SU7, described the digital experience as “fantastic” and a key reason for the threat Chinese cars pose. This seamlessness between the phone in the pocket and the screen in the dash is something legacy OEMs, with their clunky proprietary infotainment systems, have struggled to match.

Autonomous Driving

For years, Tesla’s Full Self-Driving (FSD) was considered untouchable. That lead is evaporating. Xpeng’s XNGP (Navigation Guided Pilot) and Huawei’s ADS (Automated Driving System) are now providing comparable, and in some domestic scenarios superior, performance.

In head-to-head comparisons in China, systems like Xpeng’s XNGP and Xiaomi’s Pilot have shown higher stability in complex urban environments (like roundabouts with mixed traffic) than Tesla’s vision-only solution, which struggles with local map adaptation. Xpeng uses a sensor fusion approach (LiDAR + Cameras) which provides higher redundancy and safety in China’s chaotic traffic compared to Tesla’s camera-only approach. While Tesla relies on massive data scale, Chinese firms are leveraging rapid iteration and better hardware suites (standard LiDAR on mid-range cars) to compete. The rollout of “map-less” autonomous driving by companies like Xpeng allows these vehicles to navigate cities they have never seen before, breaking the reliance on high-definition maps that previously limited the scalability of such features.

Safety and Quality: Shattering the “Cheap and Unsafe” Myth

Perhaps the most damaging legacy perception of Chinese cars was that they were “tin cans” – unsafe and poorly built. This narrative has been systematically dismantled by the European New Car Assessment Programme (Euro NCAP). The latest generation of Chinese EVs is not just meeting safety standards; it is setting them.

Between 2023 and 2025, a wave of Chinese EVs achieved top 5-star safety ratings, consistently performing at the top of their classes.

| Vehicle Model | Year | Overall Rating | Adult Occupant | Child Occupant | Vulnerable Road Users (VRU) | Safety Assist | Notes |

| Nio EL6 | 2024 | ★★★★★ | 93% | 85% | 78% | 76% | High adult occupancy score |

| BYD Seal | 2023 | ★★★★★ | 89% | 87% | 82% | 76% | Cell-to-Body technology |

| Zeekr X | 2024 | ★★★★★ | 91% | 90% | 84% | 83% | “Best in Class” Small SUV |

| BYD Dolphin | 2023 | ★★★★★ | 89% | 87% | 85% | 79% | Mass market hatchback |

| Xpeng G9 | 2023 | ★★★★★ | 85% | 85% | 78% | 78% |

The 2025 results were even more dramatic. Of 18 five-star-rated models in the latest round, 13 were Chinese-made. Nio’s Firefly achieved 96% adult occupant protection – among the highest adult occupant scores in Euro NCAP history. BMW’s i4, by contrast, received only 4 stars. Euro NCAP itself stated that Chinese manufacturers had “hit the ground running, recognizing European car-buyers will not compromise on safety.”

These scores are achieved through the extensive use of ultra-high-strength steel and the democratization of advanced safety tech. The BYD Seal, for instance, uses “Cell-to-Body” (CTB) technology where the battery pack is structurally integrated into the chassis, improving torsional rigidity and crash safety. This integration not only protects the battery but stiffens the entire vehicle platform. The consistent achievement of 5-star ratings across brands like Nio, BYD, and Zeekr demonstrates that safety engineering is now an industry-wide standard in China, effectively removing one of the last remaining barriers to consumer trust in Western markets.

Conclusion: The “Automotive Cold War” has Already Been Won

The sheer velocity of China’s rise has triggered a defensive recoil in the West. Industry captains who once dismissed Chinese competitors are now issuing stark warnings, and governments are erecting walls.

China has successfully completed its automotive industrial revolution. It has moved from a labor-arbitrage manufacturing hub to a global innovation leader. The competitive advantages held by Chinese OEMs – vertical integration of the battery supply chain, dominance in LFP and Sodium-ion chemistries, rapid “smartphone-style” manufacturing cycles, and a superior digital cockpit experience – are structural, not temporary.

The casualties on the Western side are mounting. Volkswagen’s 2025 net profit fell 44% — its worst since the 2015 diesel scandal — and the company plans to cut 50,000 jobs in Germany by 2030. GM took $5 billion in charges to restructure Chinese operations. Western automakers are collectively selling 8 million fewer vehicles in China than five years ago. Ford CEO Jim Farley warned that Chinese manufacturers “have enough capacity in China with existing factories to serve the entire North American market, put us all out of business.”

Telecommunications: The Nervous System of the New Superpower

The story repeats across industries. Take telecommunications. For decades, the narrative of Chinese technological development was one of “catch-up” – a relentless, often state-subsidized pursuit of Western standards, characterized by imitation, adaptation, and the gradual erosion of the technological frontier established by the United States, Europe, and Japan. This framework, while accurate for the era of 3G and the early days of the internet, fundamentally fails to capture the strategic reality of the 2020s. In the telecommunications sector, Beijing has not merely caught up; it has executed a structural “leapfrog,” bypassing entire generations of legacy infrastructure to establish a digital nervous system that is, in many critical metrics, superior to that of its Western rivals.

This transition from “follower” to “leader” was not accidental. It was the result of a confluence of historical accidents – specifically the underdevelopment of landline infrastructure – and deliberate strategic planning that treated connectivity not as a consumer commodity, but as a prerequisite for national survival and industrial dominance. The US is currently fighting a “Cold War” in technology against an adversary that has already won the battle for the physical layer of the internet.

The Structural Advantage of Late Adoption

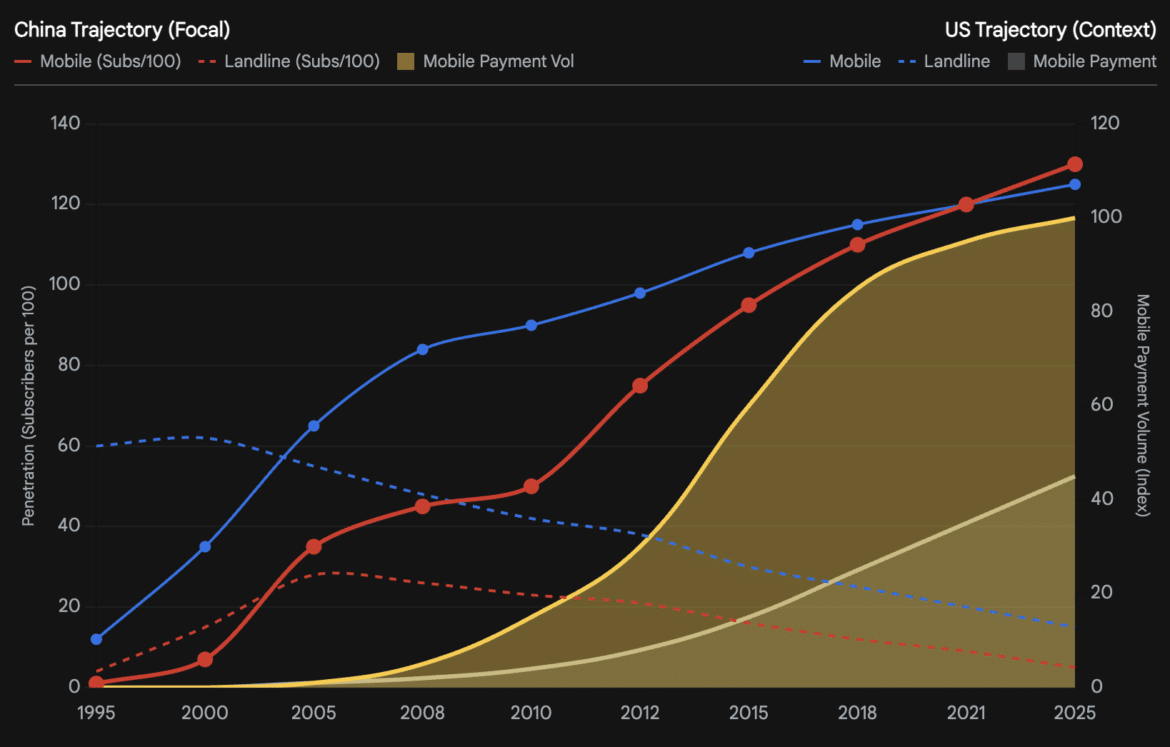

The concept of “leapfrogging” in development economics posits that lower-income nations can bypass intermediate technological stages, moving directly to advanced systems without incurring the sunk costs of legacy infrastructure. As outlined in the Leapfrog Doctrine framework, nowhere is the “leapfrogging” phenomenon more empirically verifiable than in China’s telecommunications history. Throughout the 20th century, the US and Europe invested trillions of dollars in copper-wire landline networks. This infrastructure was a marvel of its time, but by the turn of the millennium, it had become a heavy anchor – a profitable, regulated incumbent system that discouraged radical innovation.

China faced no such innovator’s dilemma. Its landline infrastructure in the 1990s was comparatively primitive, with low penetration rates outside of major urban centers. As mobile telephony technology matured, Chinese planners and consumers faced a choice: invest in the expensive, labor-intensive deployment of copper wires to every village, or skip directly to wireless towers. The choice was obvious. China moved straight to mobile, effectively substituting landlines entirely rather than augmenting them. By the early 2010s, while Western consumers were still transitioning from desktop PCs and DSL connections, the Chinese consumer base was becoming natively mobile. Statistics illustrate this divergence starkly: mobile phone penetration in China exploded, with the mobile phone becoming the primary – and often only – gateway to the internet for hundreds of millions of citizens.

This “mobile-first” population created a unique demand shock that reshaped the entire digital economy. A parallel leapfrog occurred in the financial sector. Because credit card penetration was historically low – banks were bureaucratic, state-owned, and lacked the sophisticated credit assessment systems of the West – China leaped over the “plastic card” era entirely. The transition went from a cash-based society directly to smartphone-based digital wallets. By 2017, the mobile payment ecosystem, led by Alibaba’s Alipay and Tencent’s WeChat Pay, was processing the equivalent of trillions of dollars annually.

This divergence has profound implications for the current technological rivalry. In the West, the legacy of credit cards created a fragmented payment ecosystem involving banks, card networks (Visa/Mastercard), and payment processors, all extracting fees and compartmentalizing data. In China, the consolidation of payments into mobile super-apps created a centralized, high-fidelity data stream. Every transaction – from buying a luxury car to purchasing a piece of fruit from a street vendor – generates granular data tied directly to a user’s digital identity. This data richness feeds the AI algorithms that now optimize everything from consumer credit scoring to urban traffic management, giving Chinese tech giants a structural advantage in the “data” component of the AI race.

The Strategic Pivot to Infrastructure Sovereignty

The Chinese Communist Party (CCP) recognized early that telecommunications was not merely a consumer convenience but a domain of national security. The ability to control information flow, ensure communications continuity during crises, and support a digitized military required “Infrastructure Sovereignty.” This realization drove the “Made in China 2025” initiative and subsequent Five-Year Plans to explicitly prioritize next-generation communications technology.

This state-directed investment model allowed for a deployment pace that market-driven economies struggle to match. In the United States, carriers like AT&T and Verizon must justify capital expenditure (CapEx) to shareholders on a quarterly basis. This financial discipline often delays rural deployment or density upgrades in low-profit areas. In contrast, Chinese state-owned enterprises (SOEs) like China Mobile, China Telecom, and China Unicom operate with dual mandates: they must be profitable, but they must also fulfill national strategic goals. This has resulted in a fiber-optic and mobile broadband network that covers virtually every administrative village in the country.

The ubiquity of this network is a critical differentiator. While the “digital divide” remains a persistent political and economic issue in the United States, where rural broadband access lags significantly behind urban centers, China has systematically erased this gap through state mandate. By 2021, the Ministry of Industry and Information Technology (MIIT) reported that 5G network coverage had been achieved in urban areas of all prefecture-level cities, 97% of counties, and 40% of rural towns. This number has only grown since. The integration of the rural labor force into the digital economy allows for the deployment of advanced industrial applications – like IoT sensors in agriculture and remote mining operations – in regions that would be “dead zones” in many Western nations.

This foundational ubiquity was the launchpad for Beijing’s bid to win the 5G war. It was not enough to have the technology; the state ensured they had the transmission belts to deploy it everywhere.

The 5G Fortress: Infrastructure as Geopolitics

If 4G was the era of the “App Economy” – a race won decisively by Silicon Valley software giants like Uber, Facebook, and Airbnb – 5G is the era of the “Industrial Internet.” This contest is being fought not in app stores, but in the physical world of base stations, patents, and factory floors. In this domain, the data indicates that Beijing has already secured a commanding lead, establishing a “5G Fortress” that the United States and its allies are finding difficult to breach.

The most immediate and overwhelming metric of China’s 5G dominance is the sheer volume of physical infrastructure. The numbers describe a disparity so large it represents a qualitative difference in capability. As of year-end 2025, China had deployed 4.838 million 5G base stations with 1.204 billion 5G subscribers and coverage extending to all towns and 95% of administrative villages. To understand the velocity of this deployment, consider that in the first ten months of 2025 alone, China added over half a million new 5G base stations.

The comparison with the United States is stark. While direct official comparisons are often complicated by different reporting standards, industry reports indicate that US telcos had deployed approximately 270,000 5G base stations by early 2024. Even with aggressive growth, the US total remains a fraction of China’s. China’s base stations now account for roughly 37% of all its mobile base stations, a density that is critical for the physics of 5G.

5G technology, particularly when utilizing higher frequency bands for maximum bandwidth, requires a much denser network topology than 4G. Signals travel shorter distances and are more easily obstructed. China’s willingness to blanket the country in towers – often leveraging the state-owned China Tower Corporation to manage the passive infrastructure – has created a “thick” network. While many US carriers initially relied on “Non-Standalone” (NSA) 5G, which piggybacks on 4G core networks to show a “5G” icon on a phone while delivering only marginal improvements, China has aggressively rolled out “Standalone” (SA) 5G networks.

SA 5G is the prerequisite for the true game-changing features of the technology, such as “network slicing.” This capability allows operators to carve out virtual, dedicated networks for specific applications. A hospital’s telesurgery robot, a self-driving mining truck, and a teenager streaming video might all use the same physical tower, but on an SA network, the robot and truck can be guaranteed specific latency and bandwidth parameters that the video stream cannot impact. China’s massive investment in SA infrastructure means it is the only major economy ready to support these advanced industrial applications at scale.

The Intellectual Property High Ground

Beyond the physical towers, China has secured the “high ground” of intellectual property (IP). The transition to 5G marked a historic inflection point: for the first time in the history of telecommunications, Chinese companies – specifically Huawei and ZTE – surpassed Western incumbents in holding Standard Essential Patents (SEPs).

SEPs are the foundational innovations required to implement a technical standard; they cannot be designed around. Any manufacturer building 5G equipment, anywhere in the world, must utilize these patents. According to 2024-2025 reporting, Huawei leads the global race in 5G patent families, holding approximately 12.4% to 14% of the total, effectively surpassing traditional leaders like Qualcomm and Samsung.

While Qualcomm remains a formidable competitor, particularly in terms of the “value” of its patents and its dominance in device chipsets, the sheer volume of Huawei’s contributions to the 3GPP standards body allows Beijing to shape the technical architecture of the global network. This leadership has tangible economic consequences. Huawei’s royalty revenues now exceed its payouts to other patent holders, a reversal of the historic norm where Chinese firms paid heavy “tolls” to Western IP holders.

Furthermore, the geographic concentration of IP is shifting. Chinese-headquartered companies now account for over 40% of all 5G-declared patent families globally. This creates a “patent thicket” that complicates the efforts of Western nations to “decouple” from Chinese technology. Even if a Western government bans Huawei equipment from its physical network, Western manufacturers like Ericsson and Nokia must often cross-license Huawei’s IP to build their own compliant equipment. The West can remove the Huawei logo from the box, but it cannot easily remove the Huawei innovation from the standard.

The Real Value: Industrial 5G and Vertical Integration

Western discourse on 5G often focuses on consumer benefits – faster download speeds for smartphones. In China, while consumer adoption is high (with over 1.18 billion 5G users as of late 2025), the strategic focus is decisively industrial. The deployment of 5G is viewed as a supply-side structural reform tool, integral to digitizing the “real economy.”

The concept of “5G+Industrial Internet” is not a slogan in China; it is an operational reality in sectors that are critical to the country’s economic resilience.

For example, the mining sector, historically dangerous and inefficient, has become a flagship for Chinese 5G integration. At the Yimin Open-pit Mine in Inner Mongolia, a fleet of 100 autonomous electric mining trucks operates on a private 5G-Advanced (5G-A) network. This project, launched in mid-2025, represents the world’s first large-scale vehicle-cloud-network synergy in an open-pit mine.

The 5G-A network in Yimin supports massive uplink speeds of 500 Mbps with latency as low as 20 milliseconds. This performance is critical because the trucks must stream real-time High Definition (HD) video back to a central control room. Unlike a consumer downloading a movie (downlink), an autonomous vehicle acts as a massive sensor, pushing data up to the cloud (uplink). The 5G-A network allows operators to sit in comfortable offices, far removed from the -40°C temperatures and hazardous dust of the pit. The result is a 120% increase in operational efficiency compared to manual driving and the ability to operate 24/7 without shift changes or safety breaks. Similar deployments are active in Shaanxi coal mines and Shandong gold mines, where 5G-enabled “shearing machines” and inspection robots have reduced underground personnel counts significantly, directly addressing safety and labor shortage issues.

Or consider the Port of Tianjin, one of the world’s busiest maritime hubs, where 5G networks have been integrated into the core operational loop. Staff who once spent their days sitting awkwardly in high crane cockpits, exposed to the elements, now work in remote offices, controlling massive gantry cranes via low-latency 5G links.

The automation extends to the horizontal transportation systems. The port features one of the world’s most sophisticated fleets of driverless trucks and Automated Guided Vehicles (AGVs). These vehicles rely on 5G for precise coordination to navigate the complex, high-traffic environment of a container terminal. The low latency of 5G is the safety margin; it ensures that if a sensor detects an obstacle, the stop command from the central brain reaches the vehicle instantly. This “Smart Port” model is being exported as a standard component of China’s Belt and Road Initiative infrastructure packages, further embedding Chinese telecommunications standards into global logistics.

Similar story repeats in healthcare as well. The “hierarchical medical system” in China faces a stark demographic challenge: the concentration of top-tier medical talent in wealthy coastal cities versus the needs of an aging, widely dispersed rural population. 5G is being deployed as the equalizer.

In a landmark demonstration of this capability, surgeons in Beijing utilized China Telecom’s 5G network to control orthopedic surgical robots in hospitals in Shandong and Zhejiang provinces – thousands of kilometers away. The procedure involved the remote implantation of pedicle screws into the spines of patients with fractures. The surgeons manipulated the “master” console in Beijing, and the “slave” robot in the remote hospital executed the movements in real-time.

Crucially, the success of this surgery depended entirely on the stability and low latency of the network. “Signal freezing” or feedback latency in a spinal surgery could be fatal. The 5G network maintained a stable, deterministic connection, allowing the expertise of Beijing’s top specialists to be “teleported” to provincial hospitals. This capability moves beyond the “tele-consultation” (video chat) model common in the West to true “tele-operation,” a leap made possible only by the ubiquity of the high-performance 5G grid.

The Semiconductor Defiance: The Mate 60 Pro and the Failure of Containment

In October 2022, the US imposed sweeping export controls designed to freeze China’s semiconductor capabilities. The explicit goal was to cut off access to the advanced chips required for AI and next-generation communications. The strategy hinged on a “choke point”: Extreme Ultraviolet (EUV) lithography tools manufactured by the Dutch firm ASML. These machines, the most complex ever built, are essential for efficiently manufacturing chips at the 7nm node and below. By denying China access to EUV, Washington believed it had imposed a hard technological ceiling.

That assumption was shattered in August 2023 with the silent launch of the Huawei Mate 60 Pro.

The Mate 60 Pro was released without a press conference or marketing blitz, yet it immediately became a geopolitical symbol. Inside the device was the Kirin 9000s System-on-Chip (SoC). Teardowns confirmed that the chip was fabricated by China’s Semiconductor Manufacturing International Corp (SMIC) using a 7nm-class process (specifically SMIC’s N+2 node).

This revelation sent shockwaves through the US national security establishment. The chip measured 107 mm², slightly larger than the previous TSMC-made Kirin 9000, but exhibited performance comparable to 5G flagships. More importantly, the device achieved cellular download speeds on par with 5G, indicating that Huawei had also solved the blockage on advanced Radio Frequency (RF) filters – another component the US had restricted. The Mate 60 Pro was not just a smartphone; it was a proof-of-concept for the resilience of the Chinese supply chain and the failure of the containment strategy. (We’ll cover this failure of containment in more detail further down)

The defiance has only accelerated since the Mate 60 Pro. Reports emerged in May 2025 that SMIC had produced 5nm-class chips using multi-patterning DUV techniques — without EUV lithography — though details remain unconfirmed. SMIC reportedly began testing its first domestically-built DUV lithography machine in September 2025. By December 2025, Reuters reported the prototype EUV machine in Shenzhen, with a target of functional chips by 2028. HarmonyOS NEXT now runs on over 800 million devices with 300,000+ native applications, making it the third most popular mobile OS globally at 5% market share.

The Orbital Frontier: Challenging Starlink

While 5G dominates the terrestrial landscape, China has opened a second front in the connectivity war: Low Earth Orbit (LEO). Beijing has identified SpaceX’s Starlink not just as a commercial competitor, but as a strategic threat. Starlink’s performance in the Ukraine conflict demonstrated the military value of a resilient, distributed satellite network. In response, China is accelerating its own “megaconstellations” to ensure it is not locked out of the space domain.

China’s current operational satellite network, Tiantong, relies on geostationary (GEO) satellites sitting 36,000 km above the equator. The network consists of three satellites (Tiantong-1 01, 02, 03) providing coverage across the Asia-Pacific, the Middle East, and parts of Africa. Its primary strength is reliable voice and low-speed data (text/emergency) connectivity. This network enabled the Mate 60 Pro’s headline feature: direct satellite calling without the need for a specialized external antenna.

Beijing understands that while Tiantong secures immediate “sovereign communication,” it is technologically obsolescent for the broadband era. The future lies in LEO.

To counter Starlink, China has established two primary LEO constellation projects, signaling a massive industrial ramp-up:

- Guowang (SatNet): A national plan to launch approximately 13,000 satellites. This is a centrally controlled State-Owned Enterprise project aimed at providing global broadband coverage.

- G60 Starlink (Spacesail/Qianfan): A Shanghai-backed commercial cluster aiming for a constellation of 12,000 satellites.

The G60 project has moved rapidly from planning to production. In late 2023, the first G60 commercial satellite rolled off the production line in Shanghai’s Songjiang district. The facility targets a production capacity of 300 satellites per year by 2024, with a goal to build a “full industry chain” by 2027.

| Metric | Starlink (SpaceX) | Guowang / G60 (China) | Implication |

| Orbit | LEO (~550km) | LEO (~500-1200km) | Direct competition for orbital shells. |

| Satellites Planned | 42,000+ | ~25,000 (Combined) | A race for spectrum and orbital slots. |

| Current Status | Operational (>5,000 sats) | Early Deployment / Production | China is behind but ramping up mass production. |

| Production Model | Vertical Integration | State-Cluster Model (Shanghai) | China applying “factory of the world” tactics to space. |

While China’s current production capacity lags behind SpaceX’s ability to manufacture and launch thousands of satellites annually, the trajectory is clear. China is applying its “manufacturing superpower” model to aerospace: mass production, cost reduction through supply chain integration, and state-backed financing. The goal is to occupy the limited orbital slots and frequency spectrum available in LEO, preventing a US monopoly on near-Earth space.

The Horizon: 6G and the Integrated Battlefield

Even as 5G deployment continues at a breakneck pace, Chinese research institutes are aggressively defining the next generation: 6G. The vision for 6G in China is explicitly “Military-Civil Fusion,” codified in the concept of Space-Air-Ground Integrated Networks (SAGIN).

Unlike 5G, which is primarily a terrestrial cellular network, SAGIN envisions a unified mesh network that integrates three distinct layers into a seamless whole:

- Space: LEO and GEO satellites (Guowang/Tiantong) providing global coverage.

- Air: High-Altitude Platform Stations (HAPS) and drone swarms operating in the stratosphere and lower airspace.

- Ground: Terrestrial base stations and mobile devices.

The goal is “global three-dimensional coverage”. Chinese white papers explicitly detail how SAGIN will solve the coverage gaps of 5G, providing high-bandwidth links to submarines, aircraft, and remote military outposts seamlessly. A user (or a missile) could transition from a ground tower to a drone relay to a satellite link without a break in connectivity.

The 6G Patent Lead

Just as with 5G, China is securing the IP rights for 6G early. Recent reports indicate that China holds 40.3% of global 6G patent filings, compared to 35.2% for the US This lead is driven by state-owned giants and universities – such as the University of Electronic Science and Technology of China, which has already launched the world’s first 6G experimental satellite to test terahertz communication frequencies.

This patent dominance suggests that when the global standards bodies meet to define what “6G” actually is (likely around 2025-2026 for initial standards), China will again have the loudest voice in the room. This could force Western companies to once again pay royalties to Chinese IP holders to use the next generation of wireless technology.

Military Use

The practical application of this research is already visible in the military domain. China has introduced what it claims to be the world’s first “5G military base stations”. These are not static towers, but drone-mounted aerial base stations designed to create temporary, resilient networks for battlefield operations.

Developed by China Mobile and the People’s Liberation Army (PLA), these systems are designed to support the PLA’s vision of “intelligentized warfare.” Future conflict will involve thousands of autonomous drones, robotic dogs, and unmanned ground vehicles. These assets require a high-bandwidth, low-latency mesh to coordinate swarming attacks – data loads that traditional military radio (which prioritizes range over bandwidth) cannot support. The 5G military station can support up to 10,000 users within a 3km radius, maintaining gigabit speeds even as forces move at 80km/h. This “network on the move” capability is the bridge between the digital proficiency of the Chinese telecom sector and the kinetic lethality of the PLA.

Conclusion: The “Telecommunications Cold War” is Already Being Won

The telecommunications chapter of the US-China rivalry is not a stalemate; it is currently a decisive advantage in Beijing’s favor. By leveraging the “leapfrog” advantage of a late-developing infrastructure, China has built the world’s largest and most advanced 5G network, turning the country into a vast laboratory for industrial automation.

The US strategy of “containment” via semiconductor sanctions has achieved the opposite of its intended effect. Instead of crippling China’s tech sector, it has forced the creation of a parallel, de-Americanized supply chain. The SMIC N+2 breakthrough and the Mate 60 Pro demonstrate that while the US can impose costs – making Chinese chips more expensive and harder to produce – it cannot impose a full stop.

As we look toward the Quantum era, this telecommunications foundation is critical. Quantum networks will not replace classical ones; they will ride on top of them. With a 4.8-million-strong base station network, a dominant position in 6G patents, and a burgeoning sovereign satellite capability, Beijing has built the nervous system for the next superpower. The “Cold War” in technology is being fought on the spectrum, and right now, the signal from the East is the strongest it has ever been.

The Robotics Revolution: Embodied AI and the Hardware Moat

If the rise of the Chinese NEV automotive sector represented the nation’s first successful industrial leapfrog, and the dominance of 5G telecommunications infrastructure its second, then the rapid consolidation of the robotics sector represents the third and perhaps most decisive front. While Western capital and intellectual discourse have largely fixated on the “brains” of AI – large language models (LLMs) residing in data centers – China has quietly, yet aggressively, opened a new front in the technological competition: “Embodied AI.”

This strategy is not merely an extension of industrial automation; it is a fundamental restructuring of the global manufacturing stack. It involves transplanting the “brain” of advanced AI (increasingly domestic models such as DeepSeek) into the “body” of the world’s most robust, cost-efficient, and scalable industrial robotics ecosystem. The strategic objective has shifted from automating single, repetitive tasks to creating general-purpose, humanoid and semi-humanoid workers capable of adapting to the chaotic reality of the physical world. In this “Robotics Cold War,” the available data suggests that China is not merely competing; it is establishing a “hardware moat” so deep that Western re-industrialization efforts may face insurmountable cost barriers.

The implications of this shift extend far beyond the factory floor. By controlling the physical means of production through a vertically integrated supply chain – from the lithium in the batteries to the algorithms in the control loop – China is positioning itself to be the sole supplier of the automated workforce of the 21st century.

Market Dynamics

The sheer scale of China’s robotic adoption is difficult to overstate and represents a statistical anomaly in the history of industrialization. The data indicates a profound decoupling between the Chinese market and the rest of the industrialized world. According to the International Federation of Robotics (IFR) 2025 report, China installed a record-breaking 295,000 industrial robots in 2024 alone. To contextualize this figure, it accounts for 54% of the entire global market. This is not a marginal lead; it is a hegemony that fundamentally alters the economics of manufacturing.

While installation numbers in traditional robotic powerhouses like the United States (34,200 units), Japan (44,500 units), and Germany (27,000 units) have stagnated or declined due to economic headwinds and saturation in the automotive sector, China’s deployment accelerated by roughly 5-7% year-on-year. Consequently, China is now installing more robots annually than the rest of the world combined. This divergence signals a fundamental difference in how robotics is viewed: in the West, robotics remains a capital expenditure calculation, highly sensitive to interest rates and quarterly ROI. In Beijing, robotics is viewed as a demographic necessity and a strategic imperative, insulated from short-term market fluctuations by state-directed policy instruments like the “Robot+” Application Action Plan.

This massive volume creates a self-reinforcing cycle. The high installation numbers justify massive capital expenditure in domestic manufacturing capacity for robot components, which drives down unit costs, which in turn stimulates further adoption in lower-margin industries that were previously un-automatable. This “volume game” effectively locks out competitors who cannot achieve similar economies of scale, creating a protected domestic market that serves as a launchpad for global export.

The Great Divergence: Annual Robot Installations

China now installs more industrial robots annually than the rest of the world combined.

The driving force behind this relentless accumulation of hardware is demographic. As China’s working-age population shrinks, the state is effectively substituting labor with capital – specifically, “silicon and steel.” This substitution strategy is evident in the rapid rise of “robot density” – the number of robots per 10,000 employees. This metric serves as a proxy for the technological sophistication of an industrial base.

The “Robot+” Application Action Plan explicitly targets a doubling of robot density between 2020 and 2025. This policy framework does not merely subsidize purchases; it mandates the creation of “application scenarios” – effectively guaranteeing a market for domestic robot manufacturers. By forcing the integration of robots into sectors ranging from agriculture to healthcare and construction , the state ensures that domestic manufacturers have a diverse and massive “training ground” to refine their hardware and algorithms. This state-directed demand creation mitigates the market risk for domestic robot manufacturers, allowing them to invest in R&D and capacity expansion even during economic downturns.

Robot density has reached 567 per 10,000 manufacturing workers in China, versus 449 in Germany, 307 in the United States, and 104 in the UK. China now ranks in the global top three — a position unimaginable a decade ago when it ranked 28th.

The Great Substitution

For decades, the Chinese market was the cash cow for the “Big Four” of global robotics: ABB (Switzerland), KUKA (Germany/China), Fanuc (Japan), and Yaskawa (Japan). These companies dominated the high-precision and automotive segments, leaving low-end applications to domestic firms. However, 2024 marked a historic inflection point: for the first time, domestic Chinese manufacturers captured over 57% of the local market, effectively displacing foreign leaders.

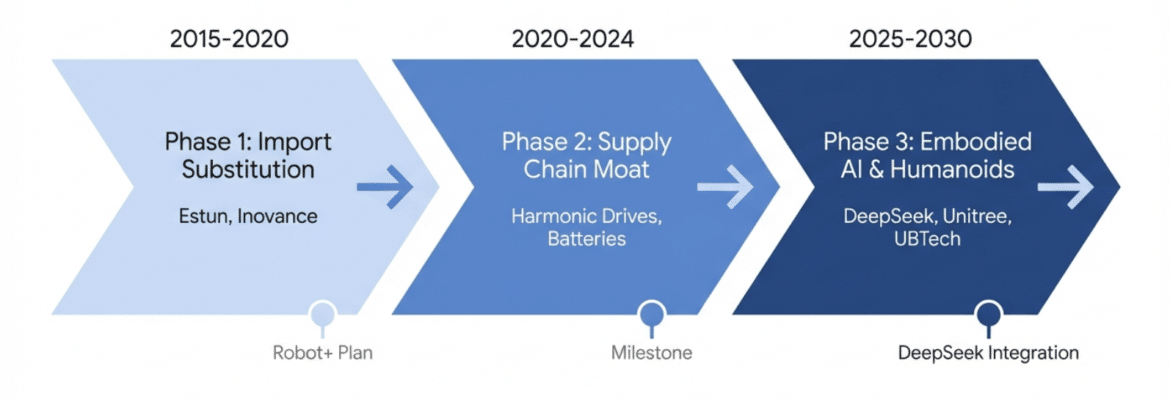

This is not accidental. It is the result of a decade-long industrial policy focused on “import substitution.” The market share of domestic firms has doubled from roughly 28% a decade ago to nearly 60% today. Companies like Estun Automation and Inovance Technology have emerged as the national champions of this transition.

This shift destroys the “premium” pricing power of Western and Japanese firms. As Chinese firms achieve “good enough” quality at 30-50% lower price points, foreign competitors are forced to either slash margins or retreat to ultra-high-end niche applications. The era of easy profits for foreign robotics firms in China is effectively over, and they now face a competitor that is rapidly expanding into their home markets in Europe and Asia.

The Bill of Materials (BOM) Advantage

The decisive advantage China holds is not just in the final assembly of robots, but in the granular control of the Bill of Materials (BOM). Robotics is, at its core, a game of high-precision components: actuators, reducers, sensors, and controllers. Historically, Japan and Germany controlled these “chokepoints,” dictating the pace of innovation and price floors. Today, China has broken them.

A 2025 analysis by Morgan Stanley provides a stark quantification of this advantage. The analysis estimated that the Bill of Materials for a humanoid robot like Tesla’s Optimus Gen 2 would be approximately $46,000 if leveraging the Chinese supply chain. However, if forced to source components strictly from outside China (e.g., US, Japan, EU), that cost would skyrocket to over $131,000.

This $85,000 delta – the “China Discount” – is an insurmountable barrier for Western re-industrialization efforts that rely on domestic hardware. It implies that any non-Chinese humanoid robot will be roughly three times as expensive to produce, rendering it economically unviable for widespread industrial deployment compared to its Chinese counterparts. This cost advantage is not merely a function of cheaper labor, but of deep industrial clustering and the commoditization of precision components.

Breaking the Harmonic Drive Monopoly

The most potent example of this supply chain victory is the Harmonic Drive (strain wave gear). These precision reduction gears are the “joints” of a robot, essential for precise movement. For decades, the market was a duopoly controlled by Harmonic Drive Systems (Japan). The high cost of these gears (often 30-40% of a robot’s total cost) was a major barrier to affordable robotics.

Chinese firms like Leaderdrive (Leader Intelligent Transmission) have cracked this precision manufacturing code. Leaderdrive now claims over 60% of the domestic market share for harmonic reducers. Technical analysis reveals that their products now achieve precision levels (≤10 arcsec) and torsional stiffness comparable to Japanese competitors, but at a fraction of the cost.

This is not low-end disruption; it is high-end commoditization. By massively expanding production capacity (Leaderdrive produces over 300,000 units annually), Chinese firms have turned a precious scientific component into a commodity. This allows downstream robot makers (like Unitree) to build robots with 20+ joints without bankruptcy-inducing costs. The ability to produce these components at scale domestically insulates the Chinese robotics industry from external supply shocks and creates a cost floor that foreign competitors cannot breach.

The Sensor and Battery Ecosystem

The robotics supply chain also benefits from the massive “exhaust” of China’s Electric Vehicle (EV) industry. The economies of scale achieved in the EV sector have created a surplus of high-performance components that are directly applicable to robotics.

- LiDAR & Vision: High-fidelity LiDAR units, once costing thousands of dollars, are now available for hundreds in Shenzhen, driven by the volume demands of the EV sector. Companies like RoboSense and Hesai have driven down the cost of 3D perception to the point where it can be integrated into consumer-grade robots.

- Batteries: The dominance of CATL and BYD in battery technology translates directly to robotics. High-density, custom-shaped battery packs needed for humanoid torsos are readily available and cheap. The energy density improvements driven by the EV market allow for longer runtimes and more powerful actuation in mobile robots.

- Actuators & Servos: Inovance’s dominance in servo motors (derived from industrial automation) ensures that the “muscles” of the robot are as cheap as the “joints”.

This supply chain supremacy means China can afford to “flood the zone” with hardware, treating robots not as precious assets to be conserved, but as commoditized consumer electronics to be deployed in swarms.

Commoditizing the Human Form

The most visible manifestation of this hardware dominance is the explosion of the humanoid robot sector. Just as DJI commoditized drones in the 2010s, Chinese firms are now commoditizing the humanoid form factor. The market has moved from “Science Projects” (expensive, fragile, research-focused) to “Consumer Electronics” (robust, cheap, mass-produced).

Companies like Unitree, AgiBot, and Fourier Intelligence are iterating at a “Shenzhen speed” that Western competitors – often burdened by academic perfectionism and venture capital cycles – struggle to match. This rapid iteration cycle is fueled by the proximity to the supply chain and a “trial by fire” mentality where products are released, tested in the real world, and improved in real-time.

Unitree Robotics delivered a shock to the global industry with the release of the G1 Humanoid. Priced at approximately $16,000 (and as low as $13,500 for base models), it offers capabilities – such as 23-43 degrees of freedom, high-torque joints, and reinforcement learning-based locomotion – that rival Western robots costing ten times as much.

This pricing strategy is not a “loss-leader” tactic; it is a reflection of the vertical integration described above. Unitree develops its own motors, reducers, and controllers in-house, bypassing the markups of Western component suppliers. The G1 is designed for mass manufacturability, using stamped parts and consumer-grade electronics rather than aerospace-grade materials. This signals the start of the “Model T” era for humanoids, where the robot becomes accessible to small and medium-sized enterprises and educational institutions.

Similarly, AgiBot (Zhiyuan Robotics), founded by former Huawei “Genius Youth” recruit Peng Zhihui (known online as “Wild Iron Man”), represents the fusion of internet speed and industrial rigor. Within nearly a year of founding, AgiBot reached a valuation of over 1 billion USD and began mass production in Shanghai.

AgiBot’s “Shanghai Factory” is already producing robots that are deployed in “vocational training” scenarios – inventory shelving, component testing, and quality control. By December 2025, AgiBot celebrated the rollout of its 5,000th mass-produced unit, a volume that dwarfs the pilot programs of most Western competitors. This rapid scaling allows AgiBot to iterate its hardware based on real-world feedback loops much faster than competitors stuck in the prototype phase. The deployment of these robots in real industrial settings creates a virtuous cycle of data collection and performance improvement.

UBTech, a Shenzhen-based veteran, has successfully transitioned from educational robots to industrial humanoids. Their Walker S1 robot has been deployed in automotive factories for Zeekr, Dongfeng Liuzhou, and Geely, performing tasks like seatbelt inspection and logo installation.

UBTech’s significance lies in its partnerships. By embedding its robots into the assembly lines of China’s massive EV manufacturers, it secures a “data pipe” of industrial tasks. This integration allows UBTech to train its algorithms on the specific, chaotic reality of a moving assembly line, a dataset that cannot be fully simulated. The collaboration with Foxconn to deepen humanoid robotics research further underscores the strategic alignment between China’s manufacturing giants and its robotics innovators.

The “Sim-to-Real” Gap and the Data Advantage

The true leapfrog, however, is not just hardware; it is the convergence of this hardware with the new generation of Chinese Large Language Models (LLMs) and Action Models. The holy grail of robotics is “Embodied AI”: robots that do not follow pre-programmed scripts but “reason” through physical tasks using generalized intelligence.

Western debate often focuses on the quality of the “Brain” (e.g., GPT-4 vs. Claude). However, in robotics, the bottleneck is often the “Body” and the “Sim-to-Real” transfer – the ability to apply digital reasoning to physical physics. Here, China has a unique advantage: Data Volume.

China has approximately 2 million industrial robots currently in operation – more than any other nation. These robots are increasingly being connected to data platforms (like RealMan’s data training center in Beijing) to generate “physics data”. Unlike text data (which is available globally via the internet), “proprioceptive data” (how a motor feels when it lifts a heavy box, how a gripper slips on oil) is proprietary and local. China’s factories are effectively becoming data centers for Embodied AI. This proprietary data moat is arguably more valuable than the public internet data used to train text models.

DeepSeek and the Reasoning Edge

In early 2025, UBTech and other domestic firms began integrating reasoning models – specifically derived from the DeepSeek architecture – directly into their humanoid platforms.

The integration of DeepSeek-R1 (a reasoning-focused model) allows robots to perform “Chain of Thought” reasoning for physical tasks. For example, instead of being programmed to “pick up box,” the robot can reason: “The box looks fragile and is slippery; I should increase grip force but move slowly to avoid crushing it”. This capability transforms the robot from a deterministic machine into an adaptive agent.

This partnership between DeepSeek (software) and companies like UBTech and Unitree (hardware) creates a closed-loop ecosystem. The robots gather physical data, which fine-tunes the DeepSeek models, which in turn makes the robots more capable. This cycle is accelerating because China is deploying these robots in real factories, not just labs. UBTech’s deployment at Zeekr’s 5G factory is a prime example of this “Swarm Intelligence” training, where robots learn to collaborate on assembly lines. The integration of these models at the edge, rather than purely in the cloud, addresses the latency and reliability issues that critical industrial applications demand.

Conclusion: The “Robotics Cold War” is Asymmetric

The “Robotics Cold War” is fundamentally asymmetric. The US and its allies view robotics largely as a difficult engineering challenge and a subset of the AI race. Beijing views it as an existential necessity to offset a shrinking workforce and a strategic imperative to maintain its status as the “World’s Factory.”

While the US focuses on high-end software and chip export controls (the “Brain”), China is monopolizing the “Body.” This creates a dangerous dependency. If Western AI models eventually need physical bodies to be useful in the real world, they may find that the only affordable, scalable bodies are made in China, run on Chinese firmware, and dependent on Chinese supply chains. This mirrors the dependency seen in 5G infrastructure, but with potentially more direct consequences for industrial capacity and defense logistics.

The “Robot+” Application Action Plan is the state’s mechanism to force this outcome. By mandating the use of robots in sectors like elderly care, agriculture, and energy, the state is essentially underwriting the R&D risk for domestic companies. This is not “free market” competition; it is a coordinated national effort to achieve dominance.

The plan also explicitly encourages “Sim-to-Real” training centers, like the one established by RealMan Robotics in Beijing, which collects data from 10 distinct scenarios (elder care, retail, etc.) to train general-purpose models. This state-backed data aggregation is a capability that fragmented Western private markets struggle to replicate. The ability to coordinate data collection across industries gives Chinese models a breadth of experience that is difficult to achieve in systems where data is siloed by competing private entities.

The implications extend beyond technology to the very nature of the global economy. If China succeeds in creating a workforce of millions of affordable humanoid robots, it effectively puts a “cap” on the cost of labor globally. It neutralizes the labor arbitrage advantage of countries like India, Vietnam, or Mexico. Why move a factory to Vietnam for cheaper labor if a Chinese factory can be staffed by $16,000 robots that work 24/7?

In this scenario, China does not just remain the World’s Factory; it becomes the World’s Automated Factory, exporting not just goods, but the means of production themselves. This export model fundamentally challenges the development strategies of emerging economies and the re-industrialization plans of developed nations.

The data is unambiguous: China has successfully executed a “hardware leapfrog” in robotics. By leveraging its massive industrial base, it has driven down costs to a level Western competitors cannot match ($16k vs. $100k+). By deploying these robots at scale (54% of global share), it is generating a proprietary dataset that fuels its Embodied AI models.

The West’s containment strategy, focused on high-end chips, has missed the mark in robotics. While the US worries about whether China can train a GPT-5 rival, China is building the millions of mechanical bodies that will perform the actual work of the 21st century. In the domain of atoms and action, the balance of power has already shifted.

Drones: The New High Ground in Tech Rivalry